Last Week:

Hang in there! We are going through the most challenging period of our lifetimes. Following the CDC guidelines and keeping a positive attitude is the best medicine to heal physically and mentally.

It was the worst week since the height of the financial crisis in October 2008, with the S&P 500 losing 14.98%. Small cap stocks continued to fare even worse with the Russell 2000 sinking 16.22% and now have shed 39.23% in 2020. The yield on the Ten-Year Treasury finished a 0.94% only one basis point lower than a week earlier, while oil plummeted, the dollar made a multi-year high, and gold slipped 2%. The coronavirus pandemic and related stock market “panic-demic” dominated the narrative. We have endured pandemics in the past, but never in an environment where machines dominate price action through high frequency algorithmic based trading, and dominate our mindset through 24/7 “news” streaming on devices that are now attached to nearly every person on the planet.

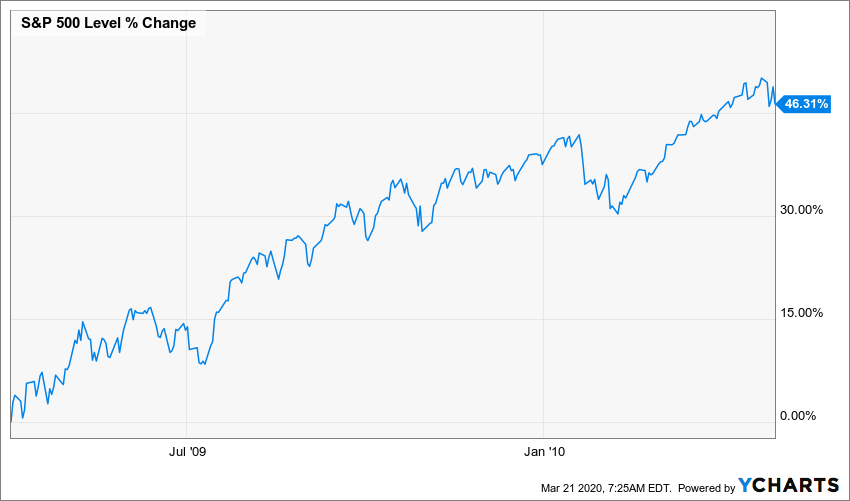

During the last pandemic in the U.S., between April 2009 and April 2010, the CDC estimates there were 60.8 million cases of swine flu, with over 274,000 hospitalizations and nearly 12,500 deaths. Here’s how the stock market performed during that time period:

It seems evident that COVID-19 is far more deadly than H1N1, and in April 2009 the market was at a very depressed level following the financial crisis, whereas valuations were quite high a month ago. Nevertheless 10 years ago we weren’t monitoring the spread of the swine flu minute by minute and the markets weren’t experiencing record volatility based on the last development. The measures being taken to combat this outbreak are now much more extreme, which means that the economy is going to take a very significant hit for an undefined period of time. On the other hand, these measures should get the health of the nation on the mend sooner. Most studies I have read suggest that if we follow the suggested guidelines then by mid-May life should be returning to normal. Government programs should help stabilize the economy, resulting in another surge in national debt- but that will be a topic for another day post-crisis. It’s impossible to predict what the stock market will do in the meantime, but it’s worth noting that for long-term investors valuations are now reasonable. Many strategists are suggesting that you can’t use P/E multiple as a guide because the E is uncertain, but I would argue that the E will nosedive like it did in 2009, but then will likely spike back and ultimately stabilize and return to its long-term trend line of approximately 6% growth.

We have often referenced the adage that the market goes up like an escalator and down like an elevator. Technology results in everything moving faster now. Hopefully the escalator ride back up will also be speedier.

This Week:

The country will be (hopefully) sitting at home, probably focusing on the latest developments of the spread of COVID-19 and the advancements from the medical community in terms of testing and treatments. The number of people testing positive is certain to rise, partially due to the slope of the spread, but also because more people are being tested. The same logic suggests that eventually the number of new cases will level off and then decline. Look at the data from China, South Korea, and the Diamond Princess as case studies for what could be the expected slope. In those cases, it took about three weeks after measures were taken to flatten the curve.

Government policy makers will also be on center stage, both in terms of issuing orders restricting travel and non-essential activities as well as authorizing massive monetary and fiscal stimulus programs. The Senate is scheduled to vote Monday on legislation that would provide a $2 trillion boost to the U.S. economy. On Monday morning the Federal Reserve unleashed a massive QE program, including buying an unlimited amount of bonds and setting up programs to ensure credit flows to corporations and state and local governments. It’s safe to assume that the markets will remain extraordinarily volatile, but keep in mind that liquid markets are efficient and already have all the known information reflected in the prices. Applying behavioral economics would suggest that the exceptions to that rule would be in bubbles and panics, and clearly, we are not in a bubble.

Stocks on the Move:

Once again, all our holdings were on the move with many prices swinging over 10% in single trading sessions. Our portfolio companies in the restaurant and casino industries were the hardest hit, as social distancing will bring their businesses to a virtual standstill for an unknown period. The decline in their share prices suggests that period will be substantially longer than our view.

Stay Optimistic:

Here are some observations courtesy of our research consultant Jim Lane:

– telecommunications infrastructure seems to be handling the related increased traffic well.

– the oil price war between Saudi Arabia and Russia is lowering the cost of energy substantially.

– the virus has reduced political partisanship rhetoric significantly (too bad that it takes a pandemic); the federal government response efforts seem coordinated, not chaotic. (Events Sunday night cast some doubt on the level of coordination which in any event took longer to materialize than one would have hoped)

– although obviously volatile, the financial markets have been orderly, and liquidity has been available; regulatory elements have largely been effective.

Congratulations if you read the whole blog. It was extra long, but I figured people might have some extra time on their hands. Send us an email and we will send you a sleeve of golf balls as a prize to use this summer when life will hopefully have returned to normal.