FAANG in Flux

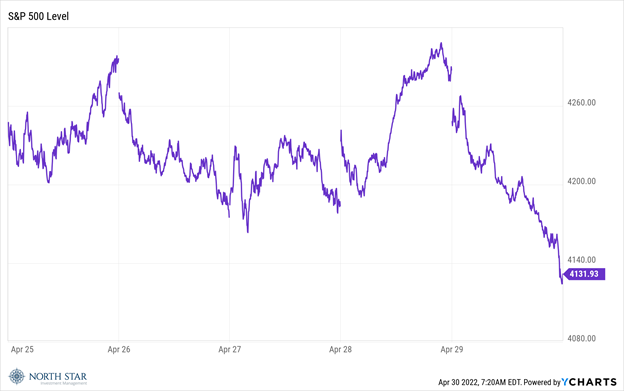

For the second week in a row, the market was slightly ahead through the Thursday afternoon coffee break only to nosedive into the weekend. By the closing bell on Friday, the S&P 500 had shed 3.27%, the Nasdaq was down 3.93%, and the Russell 2000 lost a discouraging 3.95%. The market had a “bad news is good news” rally on Thursday following a surprising report that first quarter GDP contracted 1.4% primarily driven by a sizable increase in net imports and a decline in inventories. Perhaps traders felt that the soft headline number might temper the Fed’s appetite for tightening monetary policy to cool off the economy? Friday’s sell-off seemed triggered by Amazon, which reported its slowest revenue growth rate in two decades and posted (GAAP) earnings of -$7.56 per share for the first quarter after taking a massive write-down on its investment in electric vehicle maker Rivian (RIVN). The other news Friday morning was the 5.2% surge in the Core PCE deflator, the Federal Reserve’s favorite inflation measure, an increase that was in-line with expectations.

Not only was it a difficult week, but stocks closed out their worst month in years as investors battled a host of headwinds. The Nasdaq fell 13.3% in April (its worst monthly performance since the financial crisis in October 2008), the S&P 500 sank 8.8% (its biggest monthly drop since the onset of the pandemic in March 2020) and the Russell 2000 continued to struggle ending the month down 12.6%.

Whereas there is no doubt that the current outlook is very stormy, let us all take a deep breath and look at the silver linings in the 3 storm clouds darkening the skies over Wall Street, the pandemic, the tightening monetary policy, and the war in Ukraine. The supply chain woes generated by the Covid-19 pandemic has highlighted the need to become less reliant on foreign sourcing of critical parts, as well as less “real-time” inventory-oriented given many companies we have had meetings with have indicated they will build much more significant component inventories going forward. In the long run this will increase investment in domestic production leading to more jobs and improve our trade imbalance. As our trade imbalance improves, we will become less dependent on foreign purchases of our debt and other assets. As the Fed removes the artificially low interest rates and shrinks its balance sheet, fixed income investors will finally be able to earn a reasonable return, and inflation should abate. It’s hardest to see the silver lining from the war, since it is so horrific, but it should lead to faster adoption of clean energy sources as well as promote democracy and less tolerance for aggression by totalitarian governments. That silver lining is deep inside a very dark cloud, as CNN commented “The dispiriting reality at the end of a defining week for the West and Russia is that peace in Ukraine may be further away than it has been since the invasion. And while the West can send a torrent of arms, ammunition, and aid into the country, it cannot end a war that will send painful and dangerous political, military, and economic shock waves around the world for months to come. Only Putin can do that.”

It is also worth noting that overall corporate earnings continue to grow, albeit at a slower pace. The year-over-year earnings growth rate for S&P 500 earnings increased from 6.5% to 7.1% during the week, and if Amazon was excluded then the blended growth rate for the S&P 500 would improve to 10.1%. The lower relative earnings growth rate can be attributed to a difficult comparison to unusually high earnings growth in Q1 2021 when the S&P 500 reported (year-over-year) earnings growth of 91.1%. Consistent with the earnings season for Q4 2021, when 74% of S&P 500 companies cited “inflation” and 74% of S&P 500 companies cited “supply chain” on their earnings calls, those issues continue to be highlighted this quarter, with the addition of uncertainty related to the war.

As most companies have been passing on their increased costs, revenues have remained robust with 72% of S&P 500 companies reporting revenues that are on average 2.2% above estimates. Due to these positive revenue surprises, the index has generated higher revenues for the first quarter today relative to the end of last week and relative to the end of the quarter. The blended revenue growth rate for the first quarter is 12.2% today, compared to a revenue growth rate of 11.1% last week and a revenue growth rate of 10.7% at the end of the first quarter (March 31).

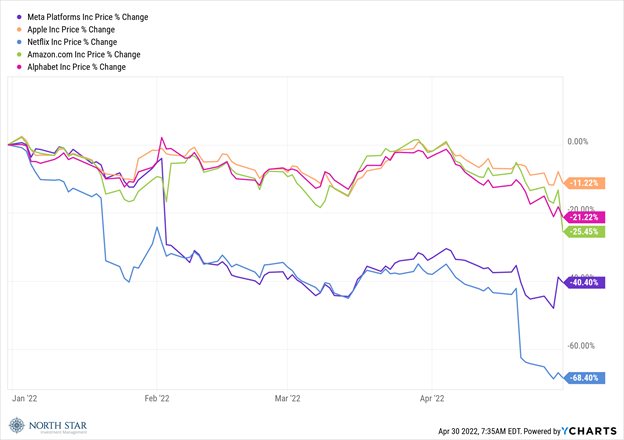

In recent years the mega-cap “FAANG” stocks have bolstered the market indexes, even during periods when the majority of stocks were struggling. In addition to Amazon, Netflix also posted surprisingly poor results last week, and as group the “FAANG” stocks have detracted from overall performance in 2022. As the chart below indicates, Apple has been the best of that group with a -11.2% return, while Netflix has been the worst at -68.4%. Microsoft and Tesla, the other trillion-dollar market cap Wall Street darlings, are both down around 17.5% year to date.

Great Debates

During the upcoming week, 160 S&P 500 companies are scheduled to report results for the first quarter.

The Fed will be in focus on Wednesday when it is expected to hike rates by 50 basis points for the first time since 2000 and give further details on the pace of reversing its large-scale asset purchases that it used to help stabilize markets during the COVID crisis.

Political analysts have suggested that Putin will be desperate to have some form of a win to celebrate before “Victory Day” on May 9. As a result, Russia could even further intensify its assaults in Ukraine during the week.

China’s manufacturing activity fell to a six-month low in April as lockdowns continued in major manufacturing hubs to stem Covid-19 outbreaks. Updates on further restrictions, or any relaxing of those restrictions, will be significant to near-term supply chain challenges.

The economic calendar includes updates on construction spending, durable goods orders, trade balance, with U.S. jobs report on Friday certainly being in focus. A net increase of 390K jobs for April is forecasted, with the unemployment rate of 3.6% remaining unchanged. A slight downtick in hourly earnings growth to 5.4% is anticipated as well and could enter the wage inflation debate.

Over the weekend, Berkshire Hathaway CEO Warren Buffett suggested that Wall Street has turned the stock market into a “gambling parlor” by encouraging speculative trading. A potential silver lining to this recent sell-off, could be that investors are reminded in the importance of the underlying fundamentals of the companies behind the ticker symbol. Whereas the value of shares in companies with no earnings might be permanently impaired and therefore should be avoided, we believe great bargain entry points are available for companies with solid earnings, balance sheets, and future growth prospects.

Stocks on the Move

-34.6% Sono Group N.V. (SEV) manufactures and sells electric cars with integrated solar cells and panels. In addition, the Company monetizes its variable battery technology for integration in numerous types of vehicles, including buses, trucks, camper vans, trains, and boats, as it aims to reduce carbon emissions and provide clean and affordable transportation for the masses. Sono’s stock slid last week after the company announced the pricing of its latest stock offering. With Berenberg, Cantor Fitzgerald & Co., and B. Riley Securities acting as book-running managers, the Company priced its follow-on offering of 10,000,000 ordinary shares at $4 per share.

-25.0% Truett-Hurst, Inc (THST) produces, sells, and markets wine. With over 14 acres of land, the Company produces a range of varietals, including Pinot Noir, Chardonnay, Sauvignon Blanc, Merlot, Cabernet Sauvignon, and Zinfandel. There was no significant company news last week. THST is a relatively illiquid stock whose share price can be influenced by very little trading activity.

-20.6% 1-800-Flowers.com Inc (FLWS) is an e-commerce provider of floral products and gifts. The Company’s product offerings include fresh-cut and seasonal flowers, plants, floral arrangements, home and garden merchandise, and gift baskets. FLWS announced disappointing earnings last week after reporting wide misses on EPS and revenue figures for the first quarter. The Company cited rising costs and softening demand as its two biggest headwinds and therefore revised FY2022 guidance.

-19.4% Accuray Inc (ARAY) designs, develops, and sells advanced radiosurgery and radiation therapy systems for the treatment of tumors throughout the body. Accuray announced FQ3 EPS of $(0.01), which beat by $0.04, and revenue of $96.2M, which beat by $0.15M. The North Star research team met with ARAY last week; our biggest takeaway was that the Company said its customers have become more willing to renegotiate on pricing as more vendors are attempting to pass along higher costs.

-13.0% Tennant Company (TNC) designs, manufactures, and sells non-residential floor maintenance equipment, floor coating, and related products. The Company’s products include scrubbers, sweepers, extractors, burnishers, buffers, floor coatings, and full-service equipment support. Tennant reported a Q1 earnings miss last week with $0.55 per share for the first quarter and revenue of $258.1M, down 2.0% Y/Y. The North Star research team meet with TNC last week; the company said it expects to see supply chain constraints, particularly for electrical components, easing in 2H 2022. On a positive note, Tennant is still the leader of innovation in its industry, and is introducing more high-tech robotics solutions that will serve a variety of end-markets.

-11.4% Hamilton Beach Brands Holding Company (HBB), through its subsidiaries, markets and designs electric household and specialty houseware appliances, as well as commercial products for restaurants, bars, and hotels. There was no significant company news last week.

-10.8% Healthcare Services Group Inc (HCSG) provides housekeeping, laundry, linen, facility maintenance, and food services. The Company offers its services to the healthcare industry, including nursing homes, retirement complexes, rehabilitation centers, and hospitals. There was no significant company news last week. The North Star research team met with the Company last week and felt positive regarding the management team’s sentiment on the pace of renegotiating contracts, pricing mechanisms in place in renegotiated contracts, and improving labor conditions given increased inbound applications.

-10.4% First Hawaiian Inc (FHB) operates as a bank holding company. The Company, through its subsidiaries, offers banking products and services such as savings accounts, personal and business loans, debit and credit cards, line of credit, certificate of deposits, mortgages, wealth management, insurance, online banking, and retirement plans. First Hawaiian fell last week after Wells Fargo cut its price target to $26 from $28 to reflect a valuation premium more in line with the broader peer group.

-18.4% Innovative Industrial Properties Inc (IIPR) owns and leases industrial real estate assets. The Company focuses on the acquisition, disposition, construction, development, and management of industrial facilities leased to tenants in the regulated medical-use cannabis industry. Last week, IIPR announced the lease amendment with PharmaCann, making $45M in funding available for building enhancements and capacity upgrades.

-13.9% Amazon.com Inc (AMZN) is an online retailer that offers a wide range of products. The Company products include books, music, computers, electronics, and numerous others. Amazon is also the dominant cloud services provider (through Amazon Web Services, or AWS), an influential entertainment company through its video streaming operations, a force to be reckoned with in grocery with its ownership of Whole Foods, and a leader in digital personal assistant devices (Alexa and Echo). Amazon’s earnings missed estimates last week as growth and cost challenges, the war, and lingering pandemic headwinds dampened the company’s retail numbers.

The stocks mentioned above may be holdings in our mutual funds. For more information, please visit www.nsinvestfunds.com.